The good news: mortality tables show even more good years ahead!

The bad news : trying to make the money last.

Consideration needs to be given to:

1- Managing a budget even tighter than before, yet not

sacrificing proper health needs and life satisfaction.

2- Conservation of assets with tax planning.

3-

Still saving some for the "rainy day" as well as the "extended" day (longer life expectancy).

4-

Keeping economic dignity and independence.

5- Increased health costs.

According to a mid '80s study by the Department of Health and Human Services:

For every 100 persons

starting their careers, by age 65.....

29 have died

13 have annual incomes below poverty level of $4,000

55 have annual incomes between $4,000 and $26,000 (median on this group is $6,100)

3 have annual incomes

over $26,000

According to the U.S. Department of Commerce:

--Less than 5% of households older than 65 are financially

independent.

--95% of persons older than 65 must rely on outside sources such as...

--45% of retirees

are dependant on relatives for some or all of their support

--30% count on Social Security to supplement them

--20%

must continue some employment

Income Sources

Differing sets of statistics are used to picture the economic status of "the

elderly." The citings usually have a purpose and usually are biased. Many politicians believe that the 20% of the population

over age 55 hold 80% of the investable (therefore spendable) assets. This makes the retirees look rich and a target for increase

taxation.

To show how some view the retirees, I have a short piece of a book report to present to you taken from:

"Within Our Reach: Breaking the Cycle of Disadvantage" by Lisbeth Schorr and Daniel Schorr:

"We are spending our

collective resources on the wrong generation. During the 1980's the government spent five times as much money on the

old as on the young. A significant proportion of these public funds went to affluent elderly...As Senator Moynahan has

pointed out, the United States has become the first society in history in which the poorest group in the population are the

children."

The authors claim that today an American six years or younger is twice as likely to be poor as a citizen

65 or older. Under Social Security, the current recipients will receive two and one half to three times more than they ever

paid in, and this book says that we need to change this trend.

"This is a luxury the nation can ill-afford...Is

it fair to spend 22.9% of the federal budget on those over age 65 with a poverty rate of 4-12%, but only 4.8% on those under

18 with a poverty rate of 17-20%?...Mother has gone to work to support grandpa and grandma, leaving no one at home to look

after the children."

The book claims that Medicare now consumes 8% of the entire federal budget, and "the United States should move

towards lightening the medical burden the elderly place on the tax-paying public. Nonetheless, the pattern in Washington has

been to slash inexpensive health programs for children while underwriting a massive expansion on Medicare. Benefits for the

elderly now comprise an item larger than national defense...By 1989, Americans under age 18 received only one dollar per capita

in federal benefits for every 11 dollars going to each American over age 65."

Various items such as presented above

would make it appear that retirees have, simply put, too much money. The problem is, however, that there does not exist a

standard "retiree;" the population within the mature ages is an extremely mixed group! Some older people are extremely poor

(some are literally living on cat food) while a small percentage hold great wealth. If there is one truth to be learned in

gerontology, it is that individuals grow more unique as they age and, therefore, it is increasingly difficult to accurately

categorize "the elderly" into any neat packages!

"Income" does not necessarily measure wealth:

1) I can have non-reportable income

in the form of goods or services rendered to me by others (ex: I can use the "company car" all I want without it costing

me)

2) I can have the benefit of assets without owning them (which again will not show up as income (ex: I can have

the company own the car)

3) I can hold a large NET WORTH and not have income (we say that farmers live poor but die rich!). On the

other hand, that large net worth can "buy" me discounts ("professional courtesy") and not need to be expressed

into reportable income.

4) As found in the Psychology of Money, the amount of income I have does not necessarily

express the amount of need I have (remember the idea of being manipulated into spending your money).

Books that look

at the income of the elderly often report their income as the "median" income for a particular group. That may be misleading.

The median is not the average (that is called mean) nor is it the income that is received most by the named group (that is

the mode). The median is simply the MIDPOINT of the distribution.

Take 5 reported incomes: If 1 person earns $2,000 per year, 1 earns $3,000 a year, 1 earns $20,000 per year, 1 earns

$22,000 per year and the last 1 earns $5,000,000 per year, what is the MIDPOINT? Simple, the 3rd person (there are 2 people

who earned less and two people who earn more). Suddenly "median" all by itself may not be very helpful. You need to know more

about the distribution to get an idea about the relative wealth of individuals.

The homeless include elderly, too.

Four major issues become apparent in the discussion of housing problems faced by the poor elderly:

1. escalation

of rents -- in 1983, the Bureau of the Census reported that 55 percent of all renters with incomes below $7,000 a year were

spending a whopping 60% or more of their incomes for rent and utilities. Part of the problem with increases in rent

is caused by increases in property taxes, which the property owner passes on to the renter.

2. rise in utility rates

-- in 1986, the average low-income household receiving energy assistance spent over 15% of its income on utilities, about

four times the national average. Between 1972 and 1984, the cost of heating with natural gas increased 500%, while residential

electric rates tripled. To add to this problem is the fact that many low income renters live in poorly built or maintained

housing, which is not energy efficient. It is estimated that in 1984, natural gas was shut off to over 1.4 million households

due to late payments.

3. decreasing availability of moderate and low-priced housing -- caused in part by renovation

of old inner cities, rather than creating housing for the poor and needy, this renovation often puts people out of their homes,

with no other affordable housing to replace it. As the area gets this "facelift", it also increases the property value

in the neighborhood surrounding it, thus effectively pricing the poor out of previously affordable housing. The conversion

of apartment buildings into condominiums also threatens the availability of housing for the poor.

4. declining government

support for the poor -- there is much less government supported housing (in the form of publicly owned housing or rental subsidies

for the poor) than there is need for such. Since only a fixed amount of federal money is earmarked for low-income housing,

and since funding levels are low, only a portion of applicants actually receive funding. Also, low-income housing is

in short supply. In 1982, the average wait for families on public housing lists was 29 months.

Reported Income Measures:

Income sources of all Elderly (according to Social Security Administration):

38%

Comes from Social Security Benefits

26% Comes from assets (Investments)

17% Comes from earnings (work)

16%

Comes from pensions (employer)

2% "Other"

1% Comes from Public Assistance (Welfare)

In general, the retirement income that is received by retired persons (beyond family help) comes from three basic

sources:

Savings/Investments --Employer programs --Government

Most individuals will receive benefits from one or more sources. Typically the more

sources, the more life satisfying retirement or "golden years" can be. The opposite is also true--the fewer the sources,

the less security and the less the opportunities. In later sections, specifics will be given about social security and

other programs.

Average Couple's Expenditures

According to AARP's Action for Independent Maturity, the

"average" couple living in a city on a "moderate" living standard spend their money (after taxes) on:

35%

housing 26% food

9% transportation

9% clothing & personal care

8% medical care 7%

"other" family expenses

6% gifts and contributions

Life Expectancy of Consumer Items

In order to better time large purchases, here is the "life

expectancy" of consumer items:

18 years Vacuum Cleaner (Upright)

17 years Wood furniture

15

years Refrigerator, freezer, stove

15 years Soft-water unit

12 years Upholstered furniture

11

years Washing Machine, TV

8-9 years Water heater

8 years Air conditioner

7 years

Rugs

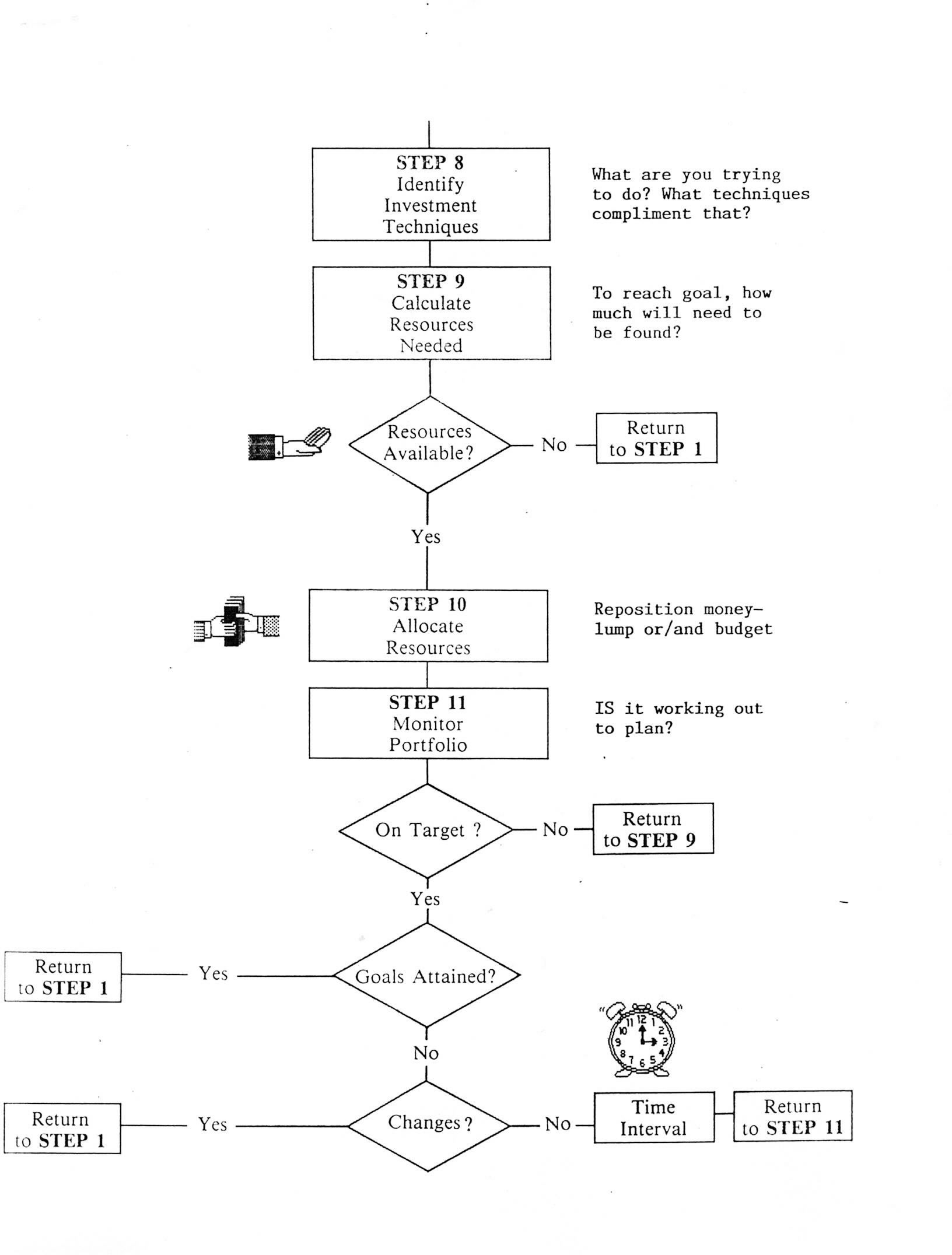

Retirement planning determines if your income sources will be able to create an adequate stream of income throughout

your retirement years. It is one thing to retire, it is another to "stay retired" with a reasonable standard of living.

Then the "big cost items" also wear out., causing further economic strain.

It is "never too late" to begin planning

nor is it "too early to start." Properly understood, the planning and control of your assets and income sources to create

and maintain a chosen life style is a PROCESS as alive and flexible as your determination allows it to be.

The first

step is to gain control of money---in your understanding of what it must accomplish for you. This is called the "psychology

of money" or "how NOT to be manipulated."

The Psychology of Money (avoiding manipulation)

Despite the media hype, the sales, and

the coupons, the power of money resides not in your pocket book, but in your mind. Examples:

-A 72 year old

"maintenance man" who by his last years of full time employment, made an annual wage of $12,000. No, he did

not inherit money nor win a lottery, but in his retirement he has the "problem" of getting rid of assets.

-A

38 year old "technical writer" earning $13,000 at his job and having already invested more than enough to

meet his goals for education of his children, his "toys", and his retirement.

The common ground between

the two examples is that they both learned to control money rather than have it control them (no--they are NOT "tight!").

They both learned early that most people actually are manipulated by media, well intentioned friends, and their own habits

to "waste" literally 15-25% of what they earn.

Proof? Think about the most economically difficult time in your

life (perhaps while going to school?). You once DID live on much less than you do now. And how did you accomplish

it? Probably by "making every penny count." To begin to win over your "psychology of money," you need to get back

to doing some consistent "counting."

Most people fail with a "budget" because it is set before the "manipulation"

is used against them. Most housewives know that the "impulse buying" at a store can break the budget. But they

don't know how to deal with "hubby" when they allow him to tag along. A husband may wonder why his wife habitually seems

to get certain things--things he may see no need for at all.

To work on both of these "counting" problems, try "the shoe

box":

--For the next three months (and do this once a year) get a receipt on EVERYTHING you buy. If you

have to create one yourself, do so.

--Three items must be listed: what you purchased (exact description), the

date, and the cost.

--Simply throw the receipts in a shoe box and forget about them until the last of the month.

At that time, arrange the receipts on your kitchen table by date.

--Now view your spending habits and see the times

you have been manipulated into buying something that, in your opinion was a waste.

--If married, do this together

to assess buying ideas.

Most people find that, in their own opinion, habits and manipulations have wasted from 15%

to 25% of their hard-earned dollars. After three months, renewed decisions usually replace this waste. What you

will save is termed "discretionary dollars" and is the greatest single source of power most people have to help out their

future.

Baffles

The business of family life is just that --a business. It deserves proper

business approaches. One of those items unfortunately often missed is that of choosing a workable cash flow system--one

consistent with your over-all goals.

In a car's gas tank, there exists several "baffles" or chambers with the

same use as those baffles found in water beds. When the car starts up a hill the baffles slow down the movement of the

gas which, due to gravity, is trying to reach the lowest level in the tank. This "slowing down" of the liquid allows

the gas pickup device time to continue supplying energy to the motor of the car and allows you to proceed on your way.

But

in many family finances, there are often either no "baffles" or too few to allow the family to reach their economic destinations.

Many advisors have noted this problem by the adage "pay yourself first". But despite this good advice, most families

have not "slowed down" their cash flow sufficiently.

One method used to help people visualize this problem is to

simply draw the "baffles" of a gas tank and begin to label, from front to back, your own system of financial controls.

The first "baffle" listed is your family checking account. That is properly the first place you go to pay the items

that keep your family momentum up. If it is abused, perhaps a second checking account should become your next

"baffle". You promise that the checking account(s) is/are the only source for normal budgeting items---like an extra

night out.

The next "baffle" is savings accounts for Christmas and the like, then savings for "short term" needs, like the new car

you want. The following baffles are labeled for "medium - term" needs, which may be goals of education, investments, retirement

funds, etc.

By listing your "baffles" in this way, you are designating funds for specific purposes. By not

allowing yourself to "transfer" funds between "baffle" areas, you "keep yourself honest" to your goals. This helps you

to "slow down" your cash flow.

"To Everything There is a Season"

As in many things in life, "first things should come first".

To help you visualize the order in which you should value your assets, the following pyramid is given:

Las Vegas Horse Racing

Commodity Trading

Venture Capital

(Money You Want to Loose!)

Gold & Silver Coins & Stamps Artworks

Gems Antiques Swiss Francs Plates

(Money You Can Afford to Loose for a Hobby)

Investment "Hedges"

Raw Land

Residential Commercial Time Shares

Real Estate Limited Partnership or Investment Trust

Real

Esate Investments (NOT your home)

(Money You Can Afford to Loose & Lose of Liquidity)

Individual Stocks (Defensive,

Common, Speculative, etc)

Individual Bonds (By Ratings: AAA,

AA, A, Baa, Ba, B, etc)

Group Investing

by Objective: Mutual Funds, Unit Trusts

Investing in the "Market"

(Money You Can Loose if You Have to Loose)

Retirement Defined Benefit, Defined

Contribution Plans

Thrift Plans, Voluntary

Plans, 401(k), TSAs, IRAs, etc.

Retirement Plans

(Money You

Simply Should NOT Risk- You Need it!)

The basic rule of thumb concerning this pyramid: In youth, try to climb up the pyramid step by step. In maturity,

begin to move down the pyramid step by step. This will become more clear to you after you finish this section and the

section on investing.

Killing the Golden Goose

To most people being in debt is emotionally trying--as it should

be. But should a person liquidate savings, use tax refunds, and other assets to remove debt as much as possible?

That

question needs to be answered in two completely different ways:

Economic Answer: Debt is always accompanied

by "rent" costs. When you borrow money, you pay the creditor a rent in the form of interest. That cost really

is not productive to you, for at most, it only helps a little on taxes and, at worst, it bankrupts you.

Psychological

answer: Being human, the debt is worrisome until finally paid off. But most people, who have been under pressure

of the difficult debt, need a "reward" for paying it off. They begin to rationalize, now that the pressure has

been removed, that they need and can afford a reward - usually in the form of an even bigger new debt!

How can the

two answers be brought together to change the "psychology of debt?"

Jack and the Beanstock tells of the Golden Goose

- a fowl that would lay wealth. Suppose Jack killed and ate the Goose? How wise would he be?

Suppose

Jack mortgaged his future egg gatherings away, and then the Golden Goose suddenly dies?

But suppose Jack patiently

awaited each egg, and then applied it both to the serving of the debt AND to saving (should the Goose suddenly die)?

What would be the outcome?

At worst, Jack would reduce the debt some and have a small savings for "future shocks."

At best, the debt would eventually be gone and the eggs could be applied fully towards savings (a habit that has now been

established).

In either case, note that new spending was ignored. A common theme among humans is that we tend to spend

as much, or more than we take in.

True financial freedom has been described as the time when your money (savings

and investments) earn more than you do. While it is true that only 5% of the American Public by age 65 find that financial

freedom, ask yourself which direction you are moving toward - freedom or bankruptcy?

When is a sale a sale?

A number of years ago a woman was in a grocery check-out stand buying

a large volume of merchandise, conspicuously items that were on sale. She was most pleased with her astuteness in finding

the sale items, and especially in picking up on canned dog food at a very substantial savings. The only problem was,

she had no dog. Many people do a similar thing with "coupons".

A simple rule of thumb: decide what you

really need first, and in what volume, then try to buy that item at the best price you can, consistent with the lowest "acquisition"

cost. Over-buying can result in waste. Large acquisition costs (like driving across town to save ten cents) can

defeat the purpose.

When habits can cost

All too often we mix our feelings of self-worth in with our possessions. Simply

matching our spending habits with technological advances can bankrupt a family. Take the example of audio equipment.

Over the last few years, new "State-of-the-Art" equipment has "out-dated" the stereo you may have, so you run out and get

the "latest" - which probably gathers more dust than actual use time.

Consider how many cars you will own over a

life-time. Could you avoid buying just one or two of them by driving the "old clunkers" just a while longer? How

much would you save? What about club memberships that you don't use often enough? Are there personal habits that cost

you both money and health? Have you added-up the yearly expense of alcohol or tobacco or over-eating?

When procrastination pays

Remembering the "market hype" and the manipulation of your emotions,

try to hold on to another simple rule of thumb:"If it is a good deal today, it should be around tomorrow as well."

We

often try to "beat the system" and find ourselves beaten instead. If a sale is so good for you that it puts the merchant

out of business, what have you gained? Both sides need to "win" so that you will have future "winning opportunities"

(not to mention servicing that which you just bought).

Most people pay both emotionally and economically high "acquisition costs" in establishing a trusting relationship

with a merchant, doctor, or counselor. Skipping around creates more costs, and may not be helpful. Just like a

company has costs in acquiring and training new employees, you have costs in acquiring new service and product vendors.

Change with care.

When increasing risk may be more profitable

You have "deductibles" on your risk management

program, (like your car, home, and health insurance.) Add up all the deductibles that could happen to you. Do

you have U.S. Savings Bonds sufficient in face amount to cover that sum?

If not, increase your Savings Bond holdings

to cover the deductibles you may face in a crisis. Then, begin to increase your deductible as you continue increasing

your savings bonds holding further. This will lower your insurance premiums at the same time you earn a safe tax-deferred

interest.

Emergency Funds

It's a wise idea to have 3 to 6 months of income put away for emergencies.

But look again at "baffles" above. Does it need to be entirely in fully - taxable low (or no) interest rates at the

bank? Often moving to a Credit Union will give a greater return, but put that "idle cash" to even more use, consistent

with "liquidity."

Some possible "Fixed - type" savings and investments include:

U.S. Savings bonds

Money Market accounts

Certificates of Deposit

High quality Municipal Bond Funds

When to pay bills

Two basic types of bills require their own answer.

For Utility,

non-revolving credit, mortgage, or credit cards that you pay completely each month (without taking "cash advances") the general

rule of thumb is to keep your money earning for you as long as possible. That means that paying these type of bills

(where there is no penalty nor increase in cost) at the last minute, is wise.

But bills of the "revolving" type compound

interest against you every single second. Holding off paying that kind of bill is only compounding your "rent"

expense. Pay them as quickly as you can - and not the "minimum" required payment either; pay as much as you can

afford to, consistent with "Killing the Golden Goose" above.

"Plastic Surgery" (cutting up and discontinuing

unnecessary credit cards) is also advisable. But if you need temporary credit and need more than one credit card, "time"

their use. Find out the "billing date" on each card. Try to make purchases with that card right after the billing

date, to gain the longest possible time before payment is due. However, some cards now start interest changes from moment

of purchase. If you need credit, shop for the best rates as well as the lowest fees and penalties.

Consolidate

You may save by consolidation of both bills and insurance policies. But

do not waste the savings! It may be possible to re-arrange your debt in a "consolidation" loan that may help

both your interest payments and cash flow. But do not then "reward yourself" (see "Killing the Golden Goose" above).

Save the savings!

In the same manner, insurance policies may be consolidated (especially life insurance) to save

the annual "policy fees." Car and home insurance may have discounts if you have them with the same company.

Keep it in the Family

You may find the "free labor" your family provides can benefit you

financially and increase family cohesiveness.

Produce: Plant a garden, bake your own bread, make

your own clothes, etc. Not only will many items be less expensive, but you pay no income tax on what you produce and

use yourself. Hold garage sales to move out unneeded items.

Maintenance: Keep ahead of spoilage,

in all consumer items. Keep the house in good repair, even if it is not the "fanciest on the block". Change your own

car's oil at least as often as suggested by the manufacturer. Maintenance will save in repair costs later.

Shift

income: One tax savings measure is to shift income to a lower-bracket tax payer in the family. Keeping

income within the family saves,too. When a grandson mows the lawn, he earns worthy service and grandpa is paying instead

of giving the money away.

"What You Really Owe Your Kids"

An excellent article, "What You Really Owe Your Kids",

found in Money Magazine, June 1988 page 157 written by Denise M. Topolnicki should be part of any retirees reading. Some specifics

mentioned in the article:

- If your adult children live with you, don't let them forget that it's your house.

- Charge live-at-home kids for room and board

- Cut the Apron strings, even if your kids are still under foot

- Set Limits

- When a child who has left home asks for subsidy, don't automatically agree

- Decide whether that artist offspring of yours is really a deadbeat dilettante

- Don't give serious amounts of money without demanding something in return

This article comes from "Family Wealth", a Money guide to retirement planning and living, available for $3.95 by

writing to:

Family Wealth

Box 999

Radio City Station

New York, NY 10101

Withholding

Taxes are a part of life. Allowing the government to collect too much

and return no interest is not recommended. Owing the government at the end of the year is also unwise. If you

owe Uncle Sam at the end of the year, you may need to borrow to pay him - NOT good. If he owes you, and sends you a nice

check, you are more likely to spend it more than once. (See "Killing the Golden Goose"). Most people will spend a refund

two or three times!

Buy Quality when you can

Many of our purchases are really just "rented." Consider

an item that you buy that gives service over a very short period before it breaks or is worn out. Your purchase, since

it did not last long, was more like rent. Why not actually rent the thing next time?

When you can afford

and need something to last, buy the best quality you can. One example is cars; What is your price per mile if

you buy a cheap car and get only a year or two of service out of it? What if you buy a better quality car and are able

to use it for a decade? Check Consumer Reports for quality before you purchase.

Finding That Lost Policy

Perhaps you suspect a deceased loved one had a life insurance

policy, but you have been unable to find it. You can ask the American Council of Life Insurance, Policy Search Department

to circulated a form for you among it's members (about 100 of the country's largest insurance companies). They will do so

and get back to you on what they find if you will include a stamped, self-addressed envelope to them with your request. Send

your request to:

Policy Search Dept.

American Council of Life Insurance

1001 Pennsylvania Ave.,

N. W.

Washington, D. C. 20004

Another service made available by the American Council of Life Insurance, the Health Insurance Association of America,

and the Insurance Information Institute, is a toll-free (1-800-942-4242) information service for questions you may have about

life, health, Medicare, and property/casualty insurance. They will also provide you, free of charge, brochures that may help.

CHAPTER 3 IN RETROSPECT:

1. Do you feel "on top of" your finances, or does it seem that

money concerns rule you?

2. Will you treat your next income tax refund any differently?

3. What steps have you taken to change your debts?

4. What plans have you made for large purchases and long term debts?

5. Are your financial habits helpful to you, or harmful?

6. Do you need to change your income tax withholdings?