Savings and investments form an important part of the retirement income picture for many people. Questions arise

upon retirement as to how assets already accumulated might change. How long assets can produce an income is also an

important concern.

How long will money last?

By the time you retire, you hopefully have

built up a "nest egg" to provide you with financial security. Your nest egg may be saved or invested

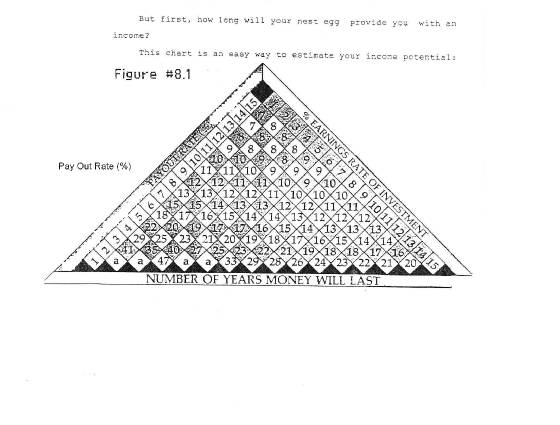

in a variety of ways that this section will discuss. But first, how long will your nest egg provide you with an

income?

The chart above is an easy way to estimate your income potential:

Using

the chart:

-Start first with your life expectancy (from exercise 9, in chapter 1). That is the number

of years your money needs to last. On this chart, those are the horizontal numbers. Say you are 65 and have 20 years life

expectancy.

-Find the interest rate on your savings on the right-hand slope of the triangle. Suppose you are earning

5%. Follow that "5% earnings rate of investment" column as it slopes left ward and down (at a 45 degree angle)

until it hits your 20 years.

-Now move perpendicular upward and left following the column until it hits the

8% on "pay out rate" (the left-hand slope of the chart).

What you have discovered is that you

may use up 8% of your total savings each year, and your money, earning a 5% return, will last just as long as you do - the

20 years of your life expectancy.

Using this chart, you may find that you can spend more of your savings

as you go than you thought. However, most people find that they cannot spend as much as they hoped. What can you

do? Perhaps, in order to make your savings last as long as you do, you may have to earn a higher rate on your money.

This probably will entail more risk than you currently are taking. The chart can then be used again to help you calculate

the interest rate you need.

Suppose you must have, as needed income, 10% of your savings each year

to live on. Start this time on the left-hand slope, and move in the 10% column down and right to 21 years. Then move perpendicular

in the column upwards and right to the 8% on the right-hand slope. You must earn 8% on your savings in this case for it to

last you at least as long as your life expectancy.

Another way to estimate the income amount

needed beyond what Social Security will provide at age 65 is to use the following Table:

Table 8.1 Initial Income

Goals in Retirement

(adapted from Economics of Aging, see Bibliography)

Pre-Retirement Income

*Needed Soc Security GAP Left

$10,000 / year

73% approx 49% 24%

15,000 / year

66% " 42% 24%

20,000 /

year

61% " 34% 27%

30,000 /

year

58% " 23% 35%

50,000 /

year

51% " 14% 37%

*Needed:

Most retirees do not need the full "pre-retirement" income amount due to:

1) taxation differences on

the money that they receive from Social Security,

2) costs associated with going to work are usually gone, and 3) often

a change of life-style lowers requirements. This, however, may be offset with higher medical costs.

The

important point of Table 8.1 is the "GAP Left" column that shows that Social Security is not sufficient in itself

(indeed was never meant to be) to cover the reasonable income requirements in retirement.

The

rest of this section is designed to help you evaluate risk in investments so you can make wise choices.

IRA's

Five major points of interest to retired people remain the same after the tax changes of 1986:

1.

The money already in an IRA remains tax deferred and still continues to earn interest.

2. Any money removed

from an IRA is fully taxable in the year it is removed. You may, however, still do tax-free "roll-overs" at

any age.

3. You must start removing IRA assets: "by April 1st the year after you turn 70 1/2 ."

You only need to remove a *portion each year. The penalty for non-compliance is 50% of the amount that you were supposed to

take out.

4. *Although the IRS has 3 different sets of rules on what amount a person over 70 1/2 must remove

from the IRA, the simplest is: If you reached 70 1/2 before 1986, you should take out 15% of the IRA's value

on Dec. 31st each year at sometime during that calendar year. If you turned 70 1/2 during 1986 or after, take out 10%.

5. Even if you have earned income, you may not add to your IRA after age 70. You still may, however, do transfers

into your IRA from other "Qualified" sources.

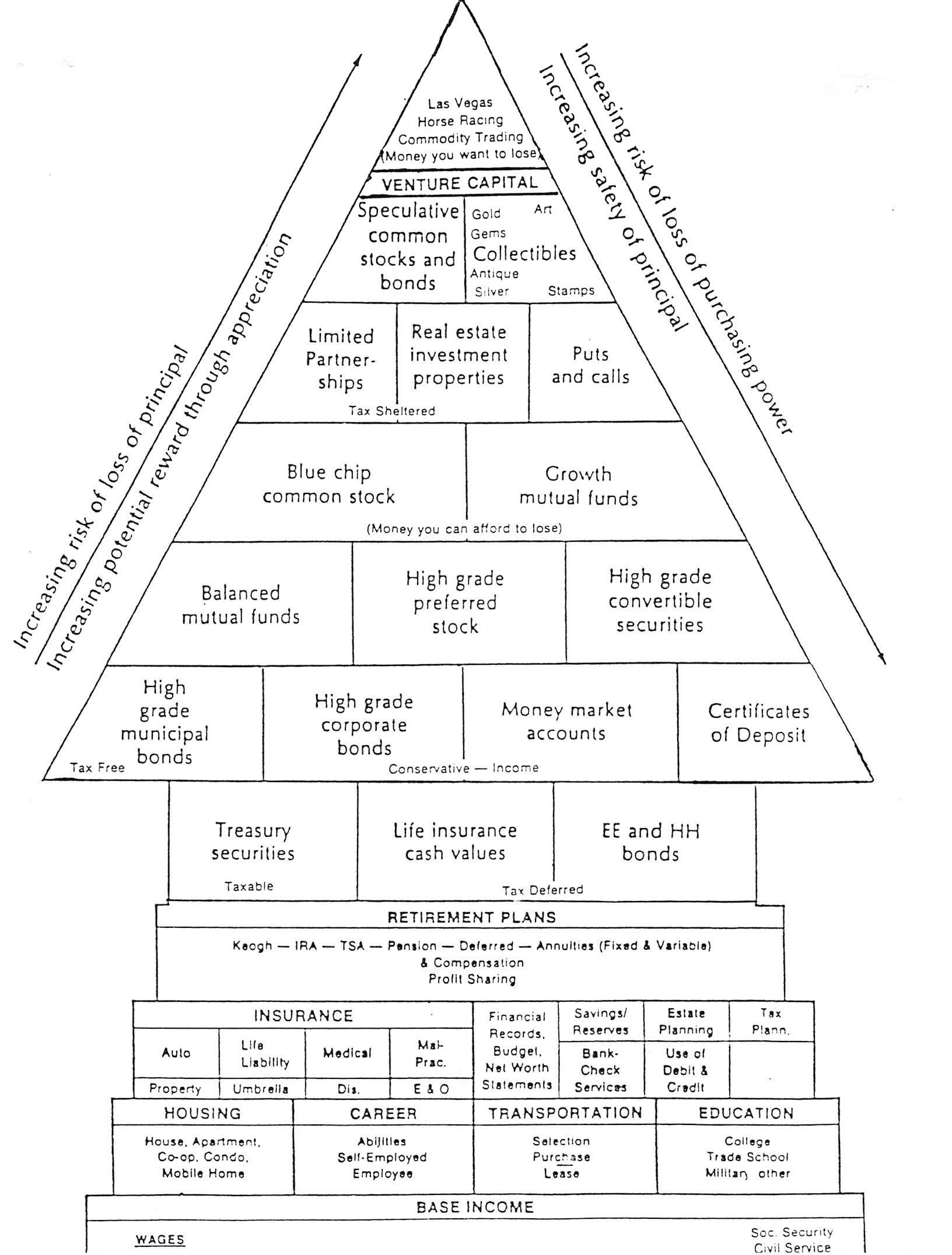

In considering what choices you have

to invest your savings: Should you "Own" or "Loan" your money?

"OWN"- INVESTMENTS

"LOAN"- SAVINGS

(Stocks, bonds, mutual funds, etc.)

(Banks, Credit Unions)

You assume investment risks

"Issuer" insulates you eg: FDIC,"guaranteed"

You receive profits/loss

You receive the stated benefit (if the "issuer" is solvent).

You exercise investment control

Issuer decides and controls investment choices

Should you invest Alone or in a Group?

When you invest in a group, it is referred to as "Pooling"--

1) YOU pass your money, along with

many others ("pooling"), to a "professional manager" whom you have chosen by matching his and your

investment objectives:

2) He, in turn, does the investing per se according to the objectives you both agreed

upon:

3) He takes a percentage of the income generated by the investment and gives you the amount of income

generated in proportion to your holdings. EXAMPLES: Mutual Funds, Bank Trust Dept., Variable Annuity Accounts,

Limited Partnerships.

Ownership Possibilities

When you invest, you may own

the asset in many different ways (Chapter 8 discusses this). Some unusual ways include:

--Investment

Clubs

--Jointly with a relative or friend

--Family Partnerships

--Revocable

Trusts (you as the trustee)

--Conservatorship (guardian)

Hard Assets

When you take an objective look at your net worth, what do you see in terms of "hard" vs "soft" assets

- and does there appear to be a proper balance between them for your situation?

We use the term "hard"

asset to label items that include gold, silver, real estate, and the like. These are assets whose value fluctuates according

to an auction market and do not in and of themselves have "babies". Let me explain - a male bar of gold and a female

bar of gold never seem to produce baby bars of gold. The value of a bar of gold is not actually known until you

find a buyer and sell it. It does not have an "interest rate" or "yield" along the way.

Appraisal

vs. Price

A few years ago, silver, an "auction-type asset" went "sky-high"

according to the newspapers in "value." For most pieces of silver (like a place setting), the appraisals actually

doubled. But upon trying to actually sell the silver for cash, a relatively small amount was actually paid (often one-half

of the appraised value!). Very often a business that has gone bankrupt, or an estate that was not prepared, find the same

thing is true. In some cases, only 10 cents on the dollar has been actually received of the appraised value, yet taxes were

assessed on the full appraised value.

Taxation of Investment Items

From time-to-time

the Government changes the taxation of various nvestment items. At times, Congress wants to encourage an industry, savings

in the bank, or whatever. They change taxation to encourage investments in the desired area. One example was the "All

Savers" accounts in the early '80's. Concerned about the housing market, Congress allowed a tax-free earnings

for two years if savings were placed in an account that would go towards mortgage financing. The hope was to attract

new money to this lagging industry. People, however, simply took current funds from pass-book accounts and C.D.'s

at the same institution and "rolled them over" into the All-savers. Very little new mortgage money was generated,

so the act was not continued.

How Fast Does Money Double?

The "Rule

of 72" will allow you to quickly estimate how fast money doubles. It is helpful in determining what inflation may

be doing against you or how a change in the interest rate on a given investment may effect you, etc.

If I am earning 10% on an investment, and do not remove any of those earned dollars to taxes, then: DIVIDE 72 by 10 AND FIND

THAT IN 7.2 YEARS (time) YOUR MONEY DOUBLES!!

If inflation is 8%, how soon will I need to get an increase

in my income to keep pace with it? DIVIDE 72 BY 8, AND YOU FIND THAT IN 9 YEARS (time) YOU WILL NEED TWICE THE INCOME

YOU HAVE NOW, JUST TO KEEP UP WITH INFLATION.

Home Equity to Income

If necessary, you

may convert your home into an income asset and still live in it. "50 plus" magazine, October 1987, had an excellent

article on this. Sell your home, but possession of it is NOT to be assumed by the buyer until after you (and your spouse)

have died. To insure you cannot be removed from the home, your names should appear with "life estate" on the

deed. In doing this, take advantage, tax-wise, of the "sale of principle residence." The buyer's

payment to you can come in many forms but typically they pay you an "annuity" for the rest of you and your spouse's

life.

In effect, you are receiving basically tax-free (return of principle) rent for living in

your own home. However, you can NOT, of course, pass on an asset to your children that you no longer own. Some

people purchase life insurance to pass an inheritance of money on to the children (instead of the home).

Investing

Making investment decisions, for most retirees, is a difficult process. This is designed to teach a

conservative approach.

It's Your Money--What Do You Want To Do With It?

(Following

Your Objectives)

#1- What do you need or want? Establish goals for your economic future.

#2- What sources do you have available?

- Can you reposition any lump sums?

- Can you find "extra" dollars from your budget?

#3 - Answer

the following questions:

- When will the funds be needed?

- Is "liquidity needed?"

- What taxation can you afford, now and later?

- How much risk do you feel you can afford?

- How are your "eggs" now? All in one basket?

(Consider the return

OF your money, then the return ON it.)

#4- What are the available alternatives for these dollars?

#5- How do you see the economy treating those alternatives?

#6- Make your choices of the alternatives.

#7- Review, Review, Review! Don't forget to review about every 3 months. Things do change:

Your objectives change,

The economy changes,

The tax laws

change

Types of Investment Risks:

Business risk:

Risk associated with the nature of the enterprise. Example: Real Estate markets, which may fluctuate due to vacancy

rates or tax changes.

Financial Risk: Risk of "leverage buying" of an asset.

The larger the loan, the greater the risk. Example: The amount you borrowed to get your home.

Interest

rate risk: Fluctuations in assets caused by fluctuation in general interest rates. Example: Return

on an old C.D. when compared with current rates available.

Purchasing power risk: Risk caused

by inflation/deflation. Example: Waiting to purchase a car in rapid-rising inflation.

Market Risk:

Risk created by other investors reactions to tangible and intangible events. Example: A run on the bank.

Opportunity

cost risk: After the investment has been made, tying up the funds, finding a better opportunity you

missed.

Since risks are ever-changing and economy ever being altered, the impact on investments

you hold, or wish to hold, must be reviewed often.

Investment Characteristics Table

Investment Sources

______Type______

___of Risk___ Taxation Liquidity Marketability

Insured checking Purch.

Power, Fully High

Redeemed by

& savings accts Interest rate

issuer

Treasury Bills Purch. Power,

Fully High Redeemed by

Interest rate

issuer

Treasury Notes Purch. Power,

Fully Moderate High

& bonds

Interest rate

Life insurance Interest rate

At death High Redeemed by

Cash Values

Business risks not taxed

issuer

Fixed-rate Purch. Power,

Deferred High Redeemed by

annuities

Interest rate

issuer

US Savings bonds Purch. Power Deferred

High Redeemed by

EE and HH bonds Interest rate

issuer

Certificates Purch. Power

Fully High Redeemed by

of Deposit

Interest rate

issuer

Mortgage-backed Purch. Power

Fully Moderate Moderate/High

securities

Interest rate

High-grade Purch. Power

Exempt OR Moderate High

Muni Bonds

Interest rate Fully

High-grade

Purch. Power Fully

Moderate High

Corporate Bonds Interest rate

Money

Markets Purch. Power

Fully High Redeemed by

Interest rate

issuer

Commercial

Purch. Power Fully

High High

paper

Interest rate

High-grade Purch. Power

Fully Moderate High

preferred stock

Interest rate

Blue-Chip Market

risk Fully

Moderate High

Common stock Business risk

Real

Estate Business risk

Fully Low Low

Investment

Prop Market risk

REIT (Real Estate Business risk

Fully Moderate High

Investment Trust) Market

risk

Puts & Calls Business risk

Fully Low High

Market risk

Speculative Business risk

Fully Low High

common stock

Market risk

Speculative Business risk

Fully Low Moderate/High

corporate bonds Financial

risk

Physical Assets Business risk Fully

Low Low

Market risk

Gold

Business risk Fully

Low Moderate/High

Futures Contracts Business risk

Fully Low High

Market risk

Balance or Asset allocation

Without a crystal ball,

no one knows exactly the economic future. To compensate for what may unexpectedly happen, most experts feel "balancing"

the portfolio the best strategy. The following examples, courtesy of "Money" magazine, August 1987, in a "Special

Report" typifies this theory (Please do not consider the following a current recommendation). Since the economy is ever

changing, the asset allocation models change also. But the idea remains the same: do not have all your money in one type of

investment, since each has it's own risks and rewards.

Typical "Asset Allocation" Model

(1987):

For Aggressive Investors"--

For "Conservative Investors"--

35% in "cash" 35%

in "growth"

30% in "growth"

30% in "cash"

15% in "growth & income"

25% in "growth & income"

10% in "international"

10% in "international"

10% in "gold"

For "Income Investors"--

For "Low Maintenance Investors"--

35% in "cash"

40% in "growth & income"

25% in "intermediate term bonds"

40% in "equity income-balance"

25% in "growth & income"

10% in "international"

15% in "government bonds"

10% in "cash"

CHAPTER 8 IN RETROSPECT:

1) In

considering investments, should you consider your own objectives as a guide?

2) Consider your next investment

by going through the 7 steps found on the first page of this chapter.

3) Will your investments

"last as long as you do?"

4) Are you going to invest independently or with a group (ex: Mutual

fund)?

5) Can you use the "rule of 72" in everyday decisions on money?

6)

What types of investment risks are you associated with at this time?

Are you

in "balance" with your investing?