Methods of Risk Control

Life at any age has it's hazards and difficulties.

In risk management, we try to define and measure the most likely problems and then decide what will be done about them. The

mental portrait that has been building throughout this text should be sharper than when you began. What do you see now?

What areas are of concern at this point?

Most people, in viewing retirement, are concerned in varying degrees about:

The risk

of health problems

The risk of income problems

The risk of leaving problems to your survivors

The risk of legal problems

The risk of tax problems

How real are these risks? The answer is somewhat personal, for there are:

Risk

Risk

Avoiders-------- Undecided--------- Takers

Depending on your viewpoint, risk can be very real in it's consequence - whether the risk actually

comes to pass or not. So understanding risk management principles comes first before discussing individual risk areas.

--

What is your average chance of having a problem, given your age and circumstances?

-- What can you do about

the risks you run?

1) Reduce the risk. Often over-looked, reducing the risk is the most

efficient of all methods. Tables that tell your life expectancy, for example, are average - not specific to you. You

can change your own individual life expectancy by following your doctor's advice and recognizing good health practices (as

shown in chapter 1 on the "Health Test").

2) Retain part of the risk. You

do this, for an example, with the deductibles you have on your car and home insurance. Once you have reasoned out your

risk potential and reduced it some, you can decide on that portion you are willing to afford (see "When increasing risks

maybe more profitable").

3) Co-op the risk. Back in the more agricultural

days, people joined together to rebuild burned down barns and the like. Today that spirit still exists, though less obvious.

It often takes the form of family members helping one another. Talk it over now, and see if the spirit of co-operation and

help is possible to help manage some of your (and their) risks.

4) Transfer the

remaining portion of the risk. This is "insurance." The idea here is to pay a company or government (Social Security

Insurance) a premium to cover the risk that you cannot manage otherwise.

It may sound funny that Social Security is an "insurance" by this definition - but it is! Originally,

in 1935, the retirement date was set at age 65 when the average life expectancy was not much over 47. The Social

Security Insurance was to cover the risk that you would live too long (longer than your savings)! If the retirement age had

been updated every time new mortality tables came out, the "normal retirement age" now would be much older than 65 - perhaps

as high as 100 years old. If that had happened, the "insurance viewpoint" of Social Security would prevail instead of the

"earned benefit" viewpoint we have today. Simply put, the government did not change the name when they changed the intent.

Covering Legal Risks

Legal insurance policies are to an attorney and client what

pre-paid medical is to a doctor and patient. But you don't have to be legally ill. You can practice preventive law.

You can have a professional respond to someone who makes a demand against you. Here are a few of the most common personal

dangers or worries needing an attorney's professional counsel and

assistance...

Preparing a will

Creditor Harassment

Neighbor Problem

Bankruptcy

Family Relations

Adoption

Criminal Threats

Domestic Problems

Suspected Theft

Property Purchase

Sexual Harassment

Landlord Abuse

Would you have used an attorney in the past year or two if you knew that all or part of the attorney's fees

would be paid?

Home Owner's Insurance

Home owner's insurance typically provides protection against

loss by fire, lightning, hail, wind, theft, and vandalism. But it also recognizes that loss from a law suit is just as threatening,

so it combines a liability coverage. This coverage is non-occupational, and does not cover auto accidents, but does cover

a variety of situations--even away from home--that you may find the

misfortune to be in.

The standard

liability coverage on most policies is only $100,000, which, in light of the law suits that we hear of on the news nearly

daily, is simply not adequate. You may, at a modest increase in premium, add further coverage limits to your existing

policy. You may also consider using an "umbrella" policy.

The basic policy covering fire, etc., also

needs to be examined. There are several types of coverage: The "HO 1" (Home Owners #1) is simply a very basic

coverage. The HO 2 expands upon HO 1 ("broad form" coverage, as it is often called). But in both of these coverage,

the policy SPECIFIES EXACTLY WHAT IT WILL COVER. It can NOT cover more. You may

find yourself with a loss, only

to find out that your insurance won't cover that specific type loss.

The "Home Owner's 3", (HO 3) or "special

form" policy covers VERYTHING EXCEPT specific occurrences (usually earthquake, flood, war, nuclear war, intentional, and YOUR

car hitting YOUR house. Your car insurance should cover that). It seems to be a safer bet, and usually is not a lot

more expensive than the other two types of policies.

Within the "Home Owner's 3" policy are usually important provisions that you also need:

1- REPLACEMENT

COST of personal property. Most policies will only give "depreciated value" on your used property. Replacement

means that you will be placed, as much as possible after the deductible, in as near the same condition after the loss as you

were before.

2- INFLATION GUARD on the building(s) itself. As you know, the building costs

to replace your structure have gone up since you bought your home---even if the resale value hasn't!

3- "FLOATERS"

that you can buy (extra premium) on your highly valued assets. You need to know that all policies have a dollar limit

to categories of assets. Your policy may only pay $250 toward cameras and camera equipment. A floater would allow

additional coverage.

If you suffer a loss, you need to be able to name ALL ASSETS that were lost to make claim for payment.

This can be very trying and difficult in the emotional time after a loss. It is HIGHLY RECOMMENDED that you create a

record NOW of your belongings and place that record in a safety-deposit box. Some people take photos, others make written

inventories, and others rent video cameras and video the entire contents of their homes.

In all three

types of "home owner" policies, the residence must be "owner occupied" (not "vacant") or , your coverage ceases after 30 days,

even though you keep paying the premium. If you plan to vacation for an extended time, you should have a house sitter. If

you are going away for an extended period, like on a mission, you may wish to rent out your home AND change

coverage to

a Dwelling Package.

Car Insurance

Car insurance, even in a "no-fault state", is required by law and

is very important. Please notice that Utah is a MODIFIED no-fault state, and that blame IS set upon the offending party (as

the law sees it) and that law suits ARE STILL part of "the game". It is possible to lose a life's savings and have wages

subject to garnishment. Here again, the liability aspect should

command your attention MORE than the "comprehensive and

collision" that repairs your own vehicle.

The suggested MINIMUM coverage should be $100,000 per person

for an occurrence and $300,000 per occurrence and $25,000 for the other car. As mentioned previously, check to see if

an "umbrella policy" will handle this as well for you. Be as generous to yourself as you have just been to the "other

guy." Get "uninsured motorist" coverage with high levels for those who

hit you withOUT coverage. Also get

"under insured motorist" to help pay your bills when the "other guy" has too little coverage to pay them (and probably too

little assets to sue him for as well.)

Most people have low deductibles on their car insurance so that

the insurance company will pay for chipped windshields, etc. You can save insurance costs by covering the "small stuff" yourself.

There are kits (about $9) you can buy to "heal" a minor chip or crack in the windshield. You can also purchase "seconds"

in new windshields, just like you can in clothes.

Remember, if a car is involved in ANY WAY (even parked in the driveway)

make claim on the car insurance. When you answer medical claims questionnaires, you will often find a question asking if cars

were involved. If so, submit the medical bill to the car insurance (and I would also submit it to the health insurance

anyway--keeps them on their toes).

Be sure to take advantage of all discounts you may have coming from good

student discounts on teens, multi-car discounts, car/home discounts, to good driver discounts. It is usually not cost-effective

to try to change companies in the middle of a covered period. If you decide to change, do it at the renewal date, having

first "checked the market" for 2-3 weeks prior.

Your CLAIM being PAID is by far more important than getting

a CHEAP RATE. Check around and see if the company you are with, or the one you are looking at, is gracious and speedy on claims

adjustments. Losses are hard enough to bear without also fighting claims people (or not hearing from them at all!).

Retirement Health Insurance

Medicare provides only basic health insurance coverage.

However, in the 1997 law, new "preventative care" provisions became active:

1- Since Jan 1998: Breast

Cancer screening (annual mamogram). Screening for vaginal and cervical cancers (pap smear and pelvic exam every 3rd year).

Colorectal cancer screening every 12 months.

2- July, 1998: Bone-density measurements for women who

are at high risk for osteoporosis. Training services begin for out-patient diabetes self-management and testing strips.

3- Jan, 2000: Prostate cancer screening (annual with PSA).

Many doctors claim that dealing with Medicare is very complex and costly, so fewer Doctors and other medical

providers accept Medicare payments as full payment for services. Consider supplementing the coverage provided by Medicare

with private health insurance. Medicare divides up the country into regions and then studies the "average" cost of services

rendered in that area. They are usually 2-3 years behind the actual cost at the time that they publish their rate tables.

This leaves providers with less reimbursement for their services than they would normally charge.

Medicare

also defines what are "allowable charges" for "medical services" after the deductibles are applied. Medicare's definition

of "medical" includes only conditions in which a patient can be "rehabilitated;" thus illnesses such as Alzhiemers Disease

are often NOT covered under the Medicare definition. Most insurance coverage that are added to Medicare ALSO use the Medicare

definitions. This leaves no coverage from Medicare or from private insurance for many conditions.

In the mid '80s and attempt to keep escalating medical costs down created a new system: Diagnosis Related

Groups (DRGs). Taking data on average hospital costs for each of many given conditions, the DRGs now specify

how much ("predetermined payment") Medicare will pay your hospital for treatment of your condition when admitted. It does

not matter how long you actually stay, the hospital is paid this predetermined amount specified by the DRGs. Only one condition

can be applied for per stay, so sometimes, people are being released one day and re-admitted the next under a different medical

condition to allow the DRGs to keep paying. However, most patients are being "pushed out quicker and sicker."

Most Medicare supplemental policies are designed to pay all or some of Medicare's deductible and co-payments. In determining

the medical services covered, remember that these policies tend to follow the same guidelines as Medicare. Medicare

pays only for services deemed to be medically necessary, at rates that they set yearly. This means that most people

Medicare

end up paying (including deductibles) an average of 35% of the total medical bill.

One option would

be a health maintenance organization (HMO). HMO's perform a dual function. They both insure health care and provide

the service. Under the HMO, you pay an insurance premium and in return receive health services directly from affiliated

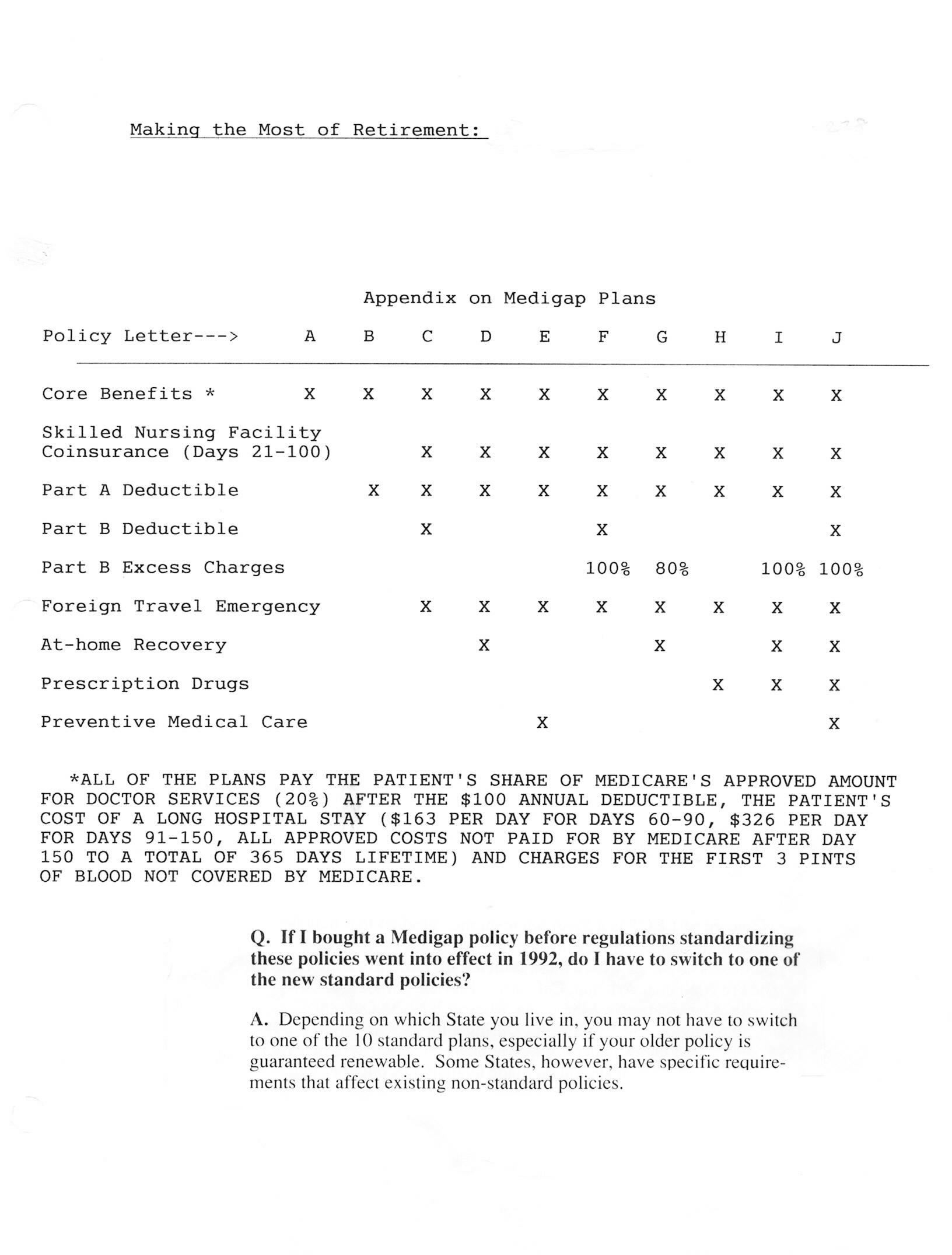

physicians or providers. Other options are "Medigap policies".

When selecting from

health insurance coverage available:

A.Do not purchase more policies than you need. Usually one

single comprehensive policy is better than several policies with overlapping or duplicate coverage. You probably do not buy

two or more car-insurance policies on the same car, and having two or more supplements to Medicare usually does not help.

B. Look for health insurance policies that are "guaranteed renewable" for life. Policies which are renewable for life generally

cannot be canceled and consequently, provide you with added protection.

C. Check the policy carefully to determine

whether it excludes coverage for pre-existing conditions. If the policy contains such an exclusion, health problems that commenced

before the policy went into effect may not be covered for a specified period of time.

D. Many policies have

some type of limit on the amount of benefits that you may receive under the policy, often expressed in terms of dollars or

numbers of days for which payment will be made. Will they cover you?

E. If you currently have health insurance,

be cautious in purchasing a replacement. New policies often impose waiting periods or contain an exclusion for those

"pre-existing conditions"-- but your current policy probably covers them.

F. Insurance law in Utah allows

you 15 or more days to review a new policy once it has been delivered to you. Known as a "free-look" provision, it allows

you to determine once again if the new policy is for you. If you change your mind, return the policy to the company

within the "free-look" period of time and your paid premium will be returned to you, as if the policy had never existed.

Nursing Home Care:

The Health Insurance Association of America indicates

that as many as 43% of those over 65 may need to enter a nursing home. The average patient's length of stay is 408 days, with:

26% staying over 12 months

22% staying 3 to 12 months

21% staying 1 to 3 months

31% staying a month or less

Nursing Home care represents the largest single health care expenditure for senior citizens, but is

the area with the least insurance coverage. In 1981, for example, Medicaid paid approximately $13 billion for nursing home

care, but patients still had to pay approximately $10 billion out of pocket! Furthermore, several studies indicate that

almost two-thirds of private patients reach the "spend down" levels required by Medicaid within six months of entering a nursing

home. In other words, assets accumulated over a lifetime are often wiped out in a relatively short period of time.

Many senior citizens carry supplemental insurance to fill the gaps in Medicare coverage. But nearly all of these policies

limit eligibility for coverage to the types of care covered by Medicare. Thus, while skilled nursing care may be covered,

intermediate and custodial care (longer that 60 days) are generally excluded - and these are likely to constitute the greatest

expense.

It is in this new context that some companies have introduced a new type of insurance policy

(LTCs), often called Nursing Home Indemnity Insurance, designed to cover skilled, intermediate, custodial and, in

some instances, home care. The new policies are not tied to the Medicare definitions of covered services. They

are written in daily indemnity form, like hospital indemnity,

and pay benefits from $20 to $100 per day. Benefits

generally are available for from one to six years (95% of all nursing home stays are no longer than four years). They often

are available to those between ages 55 and 80. This new type of coverage should be given careful consideration.

Disability Income Insurance While Employed

Disability from sickness or accident may

result in the loss of earning power. "If you are having a hard time living within your income now, imagine living without

it!" First estimate the income required to meet your expenses. The Bureau of Labor Statistics has conducted a study

to determine the amount of disability-income required for a family to keep a "similar" life-style. The findings appear

below:

Annual Gross Income %age of Gross Income Required

Up

to $29,000

80%

$29,001 to $33,000

75%**

$33,001 to $37,000

70%**

$37,001 to $42,000

65%**

Over $42,000

60%**

**Reduction below 80% should only be made if most of the disability income will be tax free when received.

Next, estimate the income sources that you can count on. Be careful not to rely on relative's

help---they maybe having the same problem as you are. Also be careful in assuming that charities or churches will be able

to help when you need it. Although they plan on helping, they also could be "drained" of resources at the time you are

in need. (Recent years and tax-law changes

have already lessened the assets available to these organizations). Once

all sources of disability-income are accounted for, find the difference. If you are like most people, you may need disability

income insurance to supplement your resources.

Benefit Crisis

According to AARP, some retirees are finding the company - paid medical insurance

premiums not being paid. The companies may be going bankrupt or otherwise refusing to pay the costs. "Three quarters

of all current workers covered by employer health programs have been promised that their health benefits will continue

when they retire," says Barbara Colman in "Defusing the benefit Crisis- Debate focuses on retiree's coverage" AARP News

Bulletin, April 1988, Vol.XXIX, No.4. She continues: "Most employers finance the benefits on a pay-as-you-go basis out

of current revenues. They don't maintain reserves, and no law requires them to provide advance funding."

Medicare premiums and benefits are changed from year to year by Congress and the budget. Some people do not have the full

40 Social Security Credits, but they can still "buy into" Medicare coverage. If they have 30 or more credits, they pay (1994)

$184 /month but if less than 30, it is $245. For all recipients, the trends have been to cut benefits, and therefore the tax-payer

costs, associated with the Medicare program. It is expected that retirees will need to provide more and more of their own

health coverage as the next 2-3 decades come upon us.

Table 7.2 Medicare in 1998 Part A buy-in with 30 or more social security quarters: $170

/mon. Less than 30: $309

Service Benefit

Medicare

Pays

Part A: Hospitalization Per Confinement All

but the 1st Day

Semi-private room & board First 60 days

$764

with general nursing &

misc hospital services & 61st - 90th day

All but

supplies, includes meals,

$191 / day

drugs, lab tests, special

care units, diagnostic

91st - 150th day All but

x-rays, operating &

$382 / day

recovery room, anesthesia,

medical supplies, and

151st day & beyond Nothing

rehabilitation services

Blood

First 3 pints

Nothing

Post-hospital Skilled Per Confinement

Nursing

Care

First 20 days

All

(Certified Facility)

Patient must have been Next 80 days

All but

in hospital at least

$95.50 / day

3 days & entered Nursing

Home within 30 days of Beyond 100 days Nothing

hospital

discharge

Part B: Medical Expenses

Doctor's Services Patient

must pay Premium: 1998 $43.80/mon

And patient $100 deductible annually

THEN Medicare is supposed to pay 80% of the "allowable" charges

Home Health Care Medicare is supposed to pay 80% of the Medically Approved" services and 80%

of the "Approved Equipment Costs"

CHAPTER 7 IN RETROSPECT:

1) Are you, generally speaking, a risk avoider, a risk taker, or somewhere

in between?

2) Consider the four ways of managing risk in a personal way. Have you used all four in dealing with your health

risks?

3) Review your auto and home insurance with your agent. Should you have legal insurance?

Should you have earthquake and/or flood insurance?

Should you have an umbrella policy?

4)

Do you have adequate health insurance coverage?

How about nursing home care?